The Best Roth IRA Tracker Spreadsheet (Free Template Inside)

Most Roth IRA Trackers Show You a Balance. A Good One Shows You a Plan.

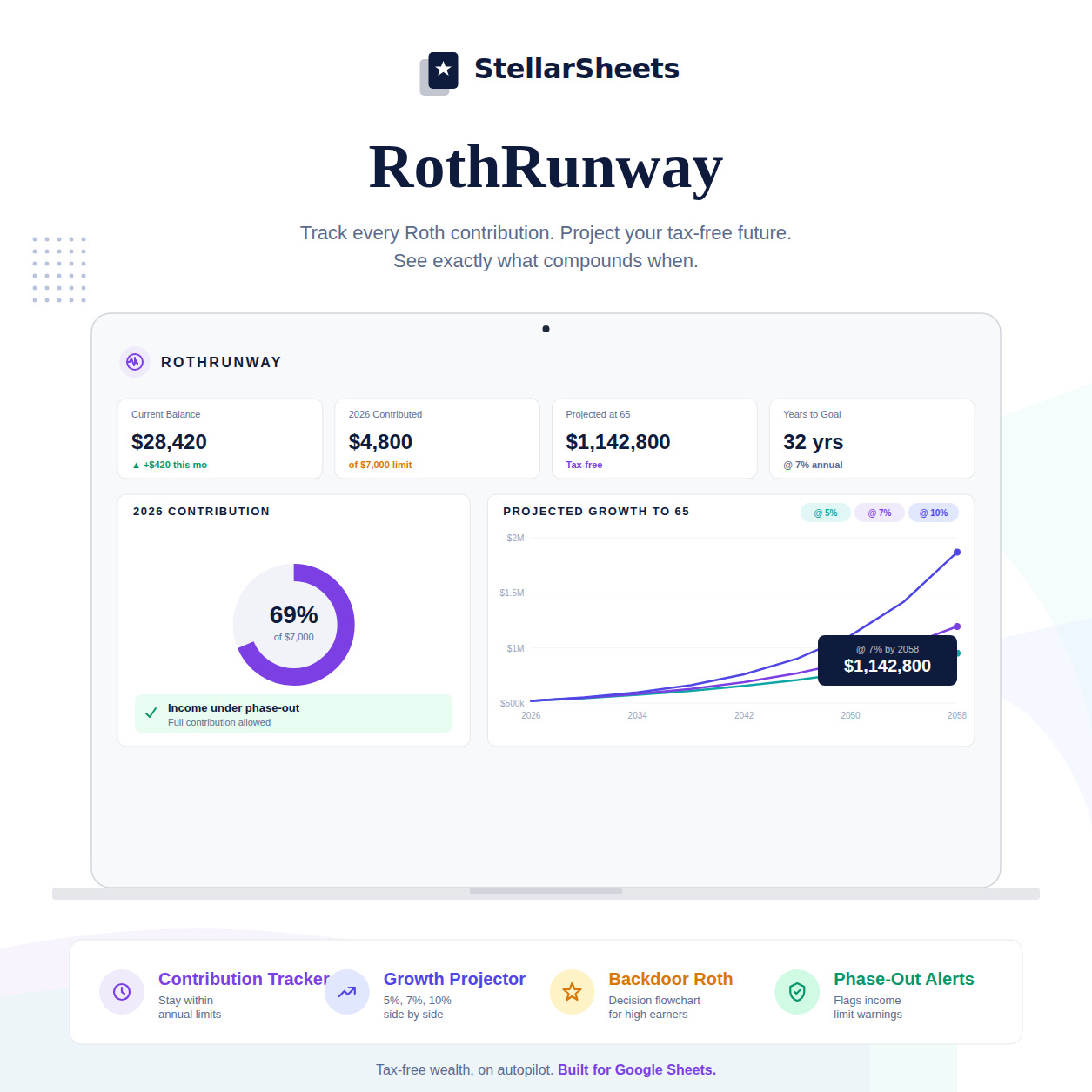

Your brokerage shows you your current balance. That's useful. But it doesn't tell you how much you've contributed this year vs. the annual limit, whether you're on pace to max out, what your balance will be at retirement if you keep contributing at your current rate, or whether your income is approaching the phase-out threshold.

Those four questions are what a Roth IRA tracker actually answers. And most people have never seen them answered in one place.

2026 Roth IRA Contribution Limits and Rules

| Detail | 2026 Amount |

|---|---|

| Standard contribution limit | $7,000 |

| Catch-up limit (age 50+) | $8,000 |

| Phase-out begins (single) | $150,000 MAGI |

| Phase-out complete (single) | $165,000 MAGI |

| Phase-out begins (married filing jointly) | $236,000 MAGI |

| Phase-out complete (married filing jointly) | $246,000 MAGI |

| Prior year contribution deadline | April 15, 2027 |

What to Track in a Roth IRA Spreadsheet

Annual contribution progress — how much you've contributed this year and how much room remains. The limit resets January 1st. You can contribute to the prior year until Tax Day.

Monthly contribution needed to max out — if you're behind, exactly what you need to contribute each remaining month to hit the limit by December 31st.

Contribution history by year — a record of every year you've contributed, partially contributed, or missed. Useful for spotting patterns and calculating your total lifetime contributions.

Income phase-out alert — if your income is growing, you need to know when you're approaching the phase-out threshold. Getting partway through the year making full Roth contributions and then discovering you're over the limit creates a tax problem.

30-year tax-free growth projection — what your current balance and contribution rate will grow to by your target retirement age, assuming a 6–7% average annual return.

The Math That Should Motivate You

Maxing out ($7,000/year) from age 30 to 65 at 7% average return: ~$1,087,000 tax-free. Contributing $200/month ($2,400/year) over the same period: ~$372,000. The difference: $715,000 — all from tracking and maxing out every year instead of setting and forgetting a $200/month contribution.

That $715,000 gap is entirely a tracking and consistency problem, not an income problem. Most people who don't max out their Roth IRA could afford to — they just don't have a system that tells them how far behind they are each month.

How to Set Up Your Roth IRA Tracker

- Log your current balance and total contributions to date

- Enter the current year's contribution limit ($7,000 or $8,000)

- Log each contribution as you make it with the date and amount

- Set a formula to calculate remaining room: limit minus YTD contributions

- Set a formula for monthly target: remaining room ÷ months left in year

- Build a projection tab: current balance + annual contributions compounded at your expected return rate

- Add an income check: flag if your MAGI is within $15K of the phase-out threshold

The Catch-Up Opportunity Most People Miss

You can contribute to the prior year's Roth IRA until Tax Day (typically April 15th). If you didn't max out last year, you have until mid-April to make up the difference. Most people don't know this. Most people leave that contribution room on the table permanently.

Set a calendar reminder every February to check your prior-year contribution status. This one habit is worth hundreds of thousands of dollars in tax-free growth over a lifetime. For a full month-by-month tracking system, see How to Max Out Your Roth IRA: A Month-by-Month Contribution Tracker.

Roth IRA vs. Traditional IRA: Which to Track

Both have the same contribution limits and the same prior-year contribution window. The key difference: Roth contributions are after-tax (no deduction now, tax-free growth and withdrawals later). Traditional IRA contributions may be tax-deductible now but are taxed on withdrawal. For most people in their 30s and 40s who expect to be in a similar or higher tax bracket in retirement, the Roth is the better long-term choice. Your tracker should reflect whichever account type you're using — or both, if you're splitting contributions.

How Roth IRA Tracking Connects to Your FIRE Plan

Your Roth IRA balance is a core component of your FIRE number calculation. Tax-free accounts are worth more than taxable accounts of the same size — because you won't owe taxes on withdrawals. When calculating your FIRE number, factor in the tax efficiency of your Roth balance vs. your pre-tax 401k balance.

Frequently Asked Questions

What is the Roth IRA contribution limit for 2026?

The 2026 Roth IRA contribution limit is $7,000 for most people, or $8,000 if you're age 50 or older. This limit applies across all your IRAs combined — traditional and Roth together.

Can I contribute to a Roth IRA if I make too much money?

Direct Roth IRA contributions phase out above $150,000 MAGI (single) and $236,000 (married filing jointly) in 2026. Above the phase-out, you can use the backdoor Roth IRA strategy: contribute to a traditional IRA (non-deductible) and then convert it to a Roth.

What happens if I contribute too much to my Roth IRA?

Excess contributions are subject to a 6% penalty tax each year they remain in the account. Remove the excess contribution (plus earnings) before your tax filing deadline to avoid the penalty.

Can I contribute to both a Roth IRA and a 401k?

Yes — Roth IRA and 401k contribution limits are completely separate. You can max out both in the same year. The 2026 401k contribution limit is $23,500 ($31,000 if 50+).

Is a Roth IRA tracker spreadsheet better than using my brokerage's tools?

Your brokerage shows your current balance and transaction history. A dedicated tracker adds contribution-limit tracking, pace-to-max-out calculations, prior-year catch-up alerts, income phase-out monitoring, and long-term tax-free growth projections — none of which brokerage platforms provide in one place.

Ready to Put This Into Action?

The math behind freedom is simple. The RothRunway – Roth IRA Tracker tracks your contributions against the annual limit, alerts you when you're behind pace, and projects your tax-free balance at retirement. Pre-built formulas, instant download, yours forever.

Or browse the full Savings & Investing Templates collection to find the right tool for your situation.

-

Posted in

google sheets, investing, retirement, roth ira, tracker