The 50/30/20 Rule Is Dead — Here's What to Use Instead

The 50/30/20 Rule Was Designed for a Different Era

Elizabeth Warren popularized the 50/30/20 rule in her 2005 book: 50% of after-tax income to needs, 30% to wants, 20% to savings and debt. It's clean. It's memorable. And for most people living in 2026, it doesn't work.

Housing alone consumes 35–45% of take-home pay in most major cities. Student loan payments eat another 10–15%. Healthcare costs have risen faster than wages for two decades. The math that worked in 2005 doesn't work when needs routinely exceed 60–70% of income before you've bought a single want.

Why Percentage-Based Rules Fail

The deeper problem with any percentage-based budgeting rule is that it ignores the most important variable: how you get paid. Monthly percentage rules don't work for bi-weekly earners. Some months you get two paychecks. Some months you get three. Bills don't care about your pay schedule.

A rule that says "spend 50% on needs" doesn't tell you which paycheck covers rent, which covers the car payment, or how much discretionary money you actually have in the second week of the month after the big bills hit in the first week.

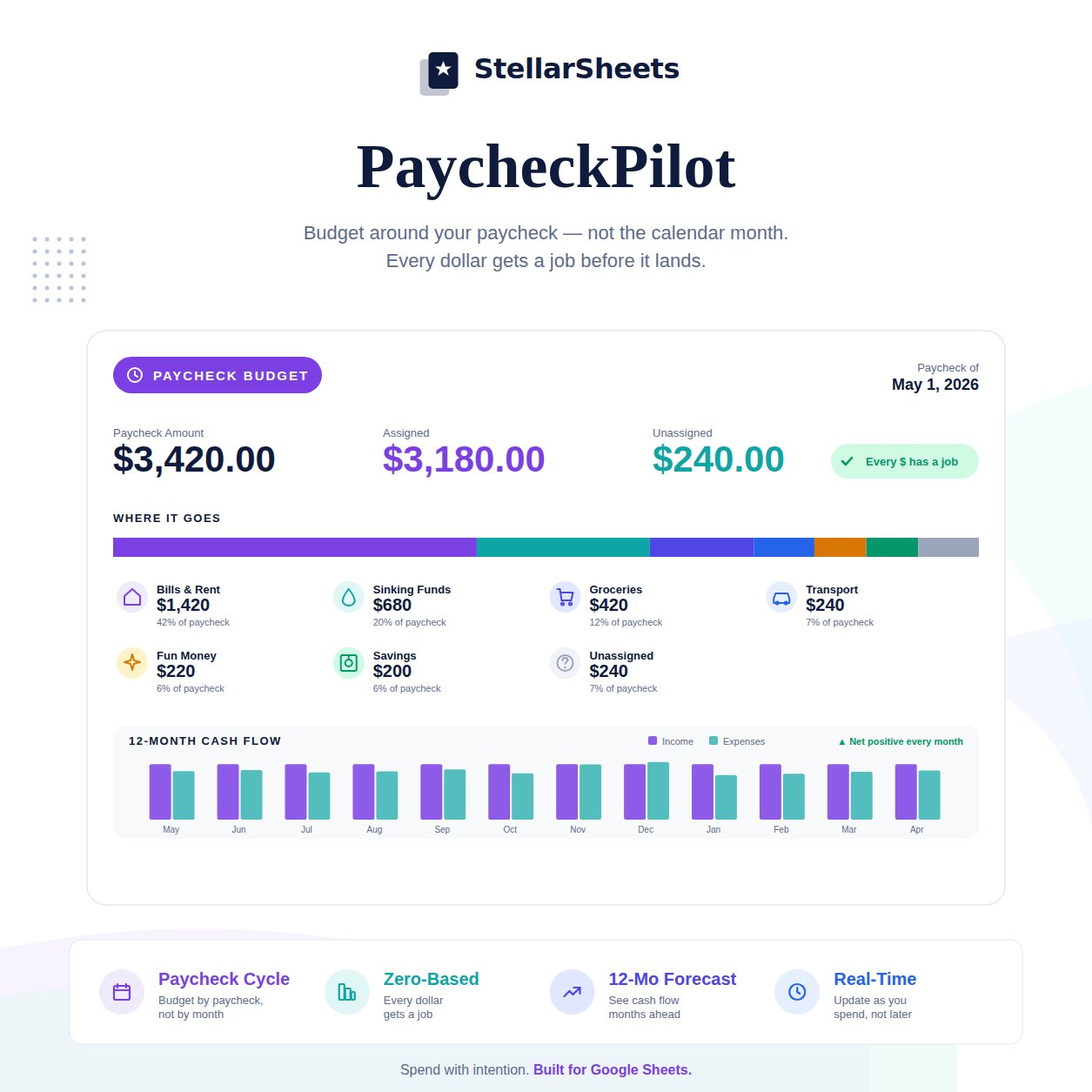

What to Use Instead: The Paycheck-Based Zero Budget

Instead of allocating percentages of monthly income, allocate every dollar of every paycheck to a specific purpose before you spend it.

- When a paycheck arrives, list every bill and expense due before the next paycheck

- Assign each bill to this paycheck or the next one based on due date

- Subtract all assigned bills from the paycheck amount

- What's left is your real discretionary money — not a percentage, a specific dollar amount

- Assign that discretionary money to categories: groceries, gas, dining, fun, savings

- End at zero — every dollar has a job

This works regardless of income level, housing costs, or debt load. It doesn't assume your needs are 50% of income. It works with whatever your needs actually are.

The Savings Question

The 50/30/20 rule says save 20%. For someone with high housing costs and student loans, that may be mathematically impossible right now. Start with a specific savings goal and a specific monthly amount. Even $100/month is a real savings rate. Automate it. Treat it like a bill. Increase it when you can.

The Bottom Line

The 50/30/20 rule is a useful starting framework for people with simple finances and average costs. For everyone else — which is most people — a paycheck-based zero budget gives you more control, more accuracy, and more flexibility to work with your actual financial situation instead of an idealized one.

Ready to Put This Into Action?

Knowing the strategy is step one. Having the right tool is step two. PaycheckPilot – Google Sheets assigns every dollar before you spend it — zero-based, paycheck-by-paycheck, with a 12-month cash flow forecast built in. Pre-built formulas, instant download, yours forever.

Or browse the full Budgeting Templates collection to find the right tool for your situation.

-

Posted in

50 30 20 rule, budgeting, money management, personal finance, zero-based budget