How to Calculate Your FIRE Number in Under 5 Minutes

Your FIRE Number Is Just Math. Here's How to Run It in Under 5 Minutes.

Financial independence has a specific number attached to it. Not a vague "enough" — a calculated target based on your spending, your expected return, and the 4% safe withdrawal rate. Once you know your number, retirement stops being a someday goal and starts being a specific milestone with a specific timeline.

Here's how to calculate it fast.

Step 1: Estimate Your Annual Retirement Spending

Use your retirement spending, not your current spending. Will you have a paid-off house? No commuting costs? Different healthcare situation? Your retirement budget may be meaningfully different from today's. Be honest — most people underestimate retirement spending by 15–20%, particularly healthcare costs which average $6,000–$12,000/year for early retirees before Medicare eligibility at 65.

If you're not sure, start with your current annual spending and adjust from there. Your net worth tracker can help you see your current spending patterns clearly.

Step 2: Multiply by 25

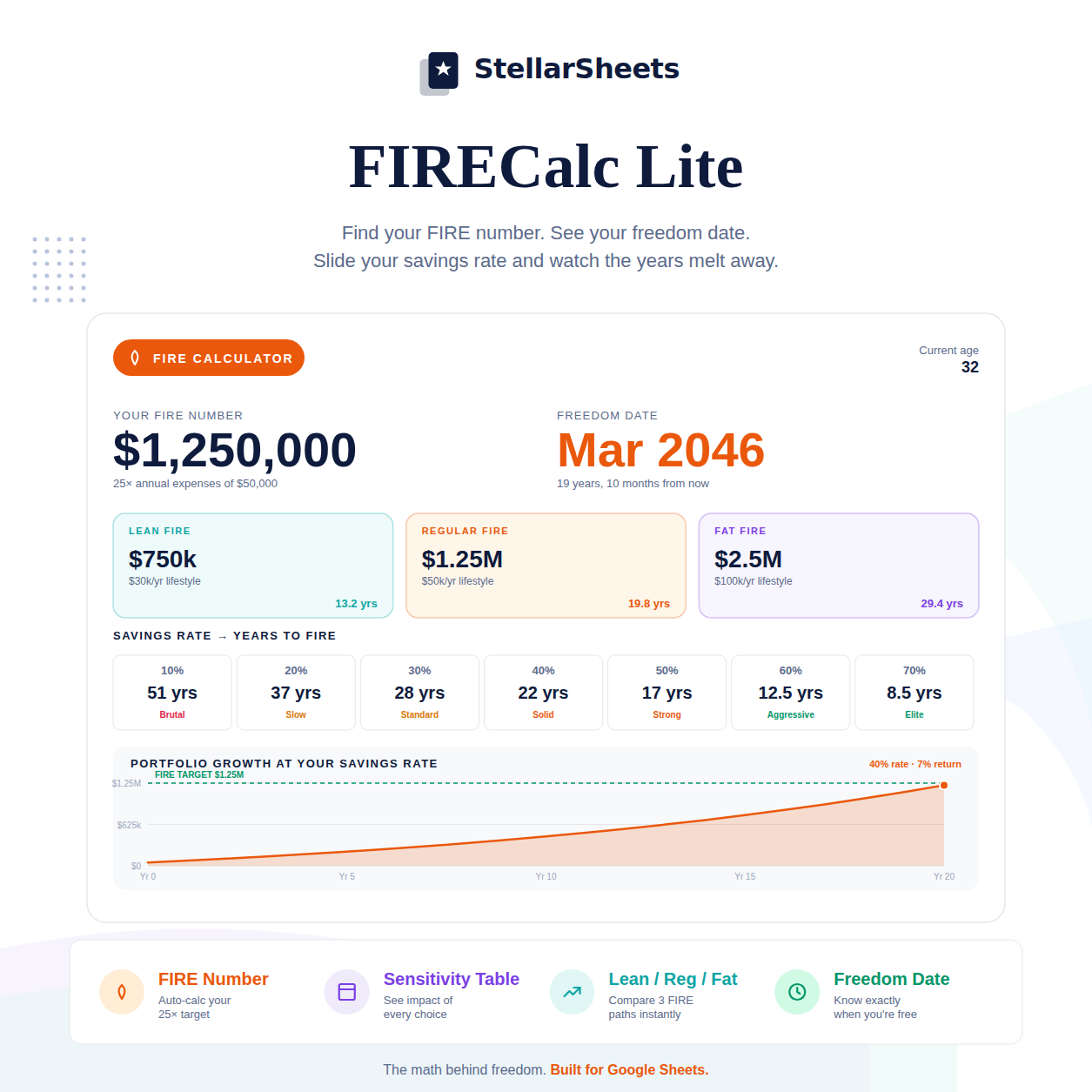

FIRE Number = Annual Retirement Spending × 25

This is the inverse of the 4% safe withdrawal rate from the Trinity Study — a landmark analysis of historical market data showing that a 4% annual withdrawal from a diversified portfolio survived 30 years in the vast majority of historical scenarios, including the Great Depression and the dot-com crash.

Examples:

$40,000/year → FIRE number: $1,000,000

$60,000/year → FIRE number: $1,500,000

$80,000/year → FIRE number: $2,000,000

Step 3: Subtract Your Current Portfolio

Your FIRE number minus your current invested assets = the gap you need to close. This is the number your savings rate and investment returns are working against. Track this gap monthly with a net worth tracker so you can see it shrinking over time.

Step 4: Calculate Your Timeline

How long until you close the gap depends on two variables: how much you save each year and what return your investments earn. At 7% real return:

- Saving $20,000/year with a $200,000 portfolio → ~18 years to $1M FIRE number

- Saving $30,000/year with a $200,000 portfolio → ~14 years to $1M FIRE number

- Saving $50,000/year with a $200,000 portfolio → ~10 years to $1M FIRE number

The savings rate is the biggest lever. Increasing it by 10% doesn't just add more money — it also reduces your FIRE number (because you're spending less). This double effect is why savings rate improvements are so powerful for FIRE timelines.

Step 5: Stress-Test the Assumptions

Run the same calculation at 5% return instead of 7%. Run it at a 3.5% withdrawal rate instead of 4% (better for 50-year retirements — see our guide on how long your money will last in retirement). See how sensitive your timeline is to these assumptions. If the deal only works under perfect conditions, adjust your savings rate or spending target.

The Role of Other Income in Your FIRE Number

Social Security, rental income, and part-time work all reduce your required portfolio. Every $1,000/month in guaranteed income reduces your FIRE number by $300,000 (at 4% withdrawal rate). A freelancer earning $2,000/month in retirement from consulting needs $600,000 less in their portfolio than someone with zero other income. Factor this in before assuming you need the full 25x number.

The 5-Minute Version

Annual spending × 25 = FIRE number. FIRE number minus current portfolio = gap. Gap ÷ annual savings = rough years to FIRE (ignoring returns). Add investment returns and you get a more precise timeline. That's it. Five minutes, one number, one target.

Frequently Asked Questions

What is a FIRE number?

Your FIRE number is the total investment portfolio value needed to retire and live off investment returns indefinitely. It's calculated as your annual retirement spending multiplied by 25, based on the 4% safe withdrawal rate.

Is the 4% rule still valid in 2026?

The 4% rule remains a widely used benchmark, though some financial planners recommend 3.5% for retirements longer than 30 years due to current valuation levels and lower expected future returns. For early retirees with 40–50 year horizons, 3.5% provides a meaningful additional safety margin.

How do I calculate my FIRE number if I have irregular income?

Use your average annual spending over the past 2–3 years as your retirement spending estimate. If your spending is highly variable, use the higher end of your range to build in a safety margin.

What's the difference between lean FIRE, regular FIRE, and fat FIRE?

Lean FIRE targets a minimal lifestyle (typically under $40,000/year in spending, requiring ~$1M). Regular FIRE targets a comfortable middle-class lifestyle ($50,000–$80,000/year). Fat FIRE targets a high-spending lifestyle ($100,000+/year, requiring $2.5M+).

How do I track progress toward my FIRE number?

Track your net worth monthly and compare it to your FIRE number. The gap closing over time is your progress metric. A FIRE calculator spreadsheet can project your freedom date and update it automatically as your portfolio grows.

Ready to Put This Into Action?

The math behind freedom is simple. The FIRECalc Lite – FIRE Number Calculator calculates your FIRE number, projects your freedom date, and lets you stress-test every savings rate and return assumption — all in one pre-built Google Sheet. Instant download, yours forever.

Or browse the full Savings & Investing Templates collection to find the right tool for your situation.

-

Posted in

calculator, financial independence, FIRE, google sheets, retire early