Why You're Not Saving Money (And It's Not Because You Don't Earn Enough)

The Savings Problem Almost Nobody Talks About Honestly

The standard advice for people who aren't saving enough: earn more, spend less. It's not wrong. But it's incomplete — and for most people, it's not the actual problem.

The actual problem is structural. Not motivational, not mathematical. Structural. The way most people manage money makes saving the last thing that happens, which means it's the first thing that gets skipped when life gets in the way.

Why "I'll Save What's Left" Never Works

The most common savings approach: pay bills, spend on living expenses, save whatever's left at the end of the month. The problem: there's almost never anything left. Not because the math doesn't work — but because spending expands to fill available money. Parkinson's Law applied to personal finance.

The fix isn't willpower. It's structure. Specifically: savings has to come out first, before discretionary spending, not after.

The 5 Real Reasons People Don't Save

1. No specific savings target. "Save more" is not a goal. "Save $8,000 for an emergency fund by December" is a goal. Without a specific number and deadline, savings is always optional.

2. No automatic mechanism. Manual savings requires a decision every month. Decisions get skipped. Automation removes the decision — the money moves before you can spend it.

3. No visibility into progress. If you can't see how close you are to your goal, the goal doesn't feel real. A tracker that shows 43% complete is more motivating than a bank balance that just sits there.

4. Competing goals pulling from the same pool. Emergency fund, vacation, car repair, holiday gifts — all competing for the same dollars with no system to allocate between them. The most urgent one always wins. The others stall indefinitely.

5. The savings amount is too ambitious. Setting a $1,000/month savings goal when your budget realistically supports $200 guarantees failure. Start with what's actually achievable. Consistency at $200/month beats sporadic attempts at $1,000.

The System That Actually Works

Step 1: Set a specific goal with a specific deadline. Amount, purpose, date. Not "save more" — "save $5,000 for an emergency fund by October 1st."

Step 2: Calculate the monthly contribution needed. ($5,000 minus current savings) ÷ months remaining. That's your monthly target.

Step 3: Automate the transfer on payday. The money moves to savings before you see it in your checking account. What you don't see, you don't spend.

Step 4: Track progress visually. A progress bar at 60% complete is more motivating than a number. See the goal getting closer every month.

Step 5: Treat the savings transfer like a bill. It's not optional. It's not "if there's money left." It's a fixed obligation that comes out first.

The Income Objection

"I'd save more if I earned more." Maybe. But research consistently shows that savings rates don't automatically increase with income — lifestyle inflation absorbs the raise. The people who save consistently at $50,000/year are usually the same people who save consistently at $100,000/year. The habit precedes the income, not the other way around.

Start with whatever you can save right now. Even $50/month. The habit is the point. The amount scales later.

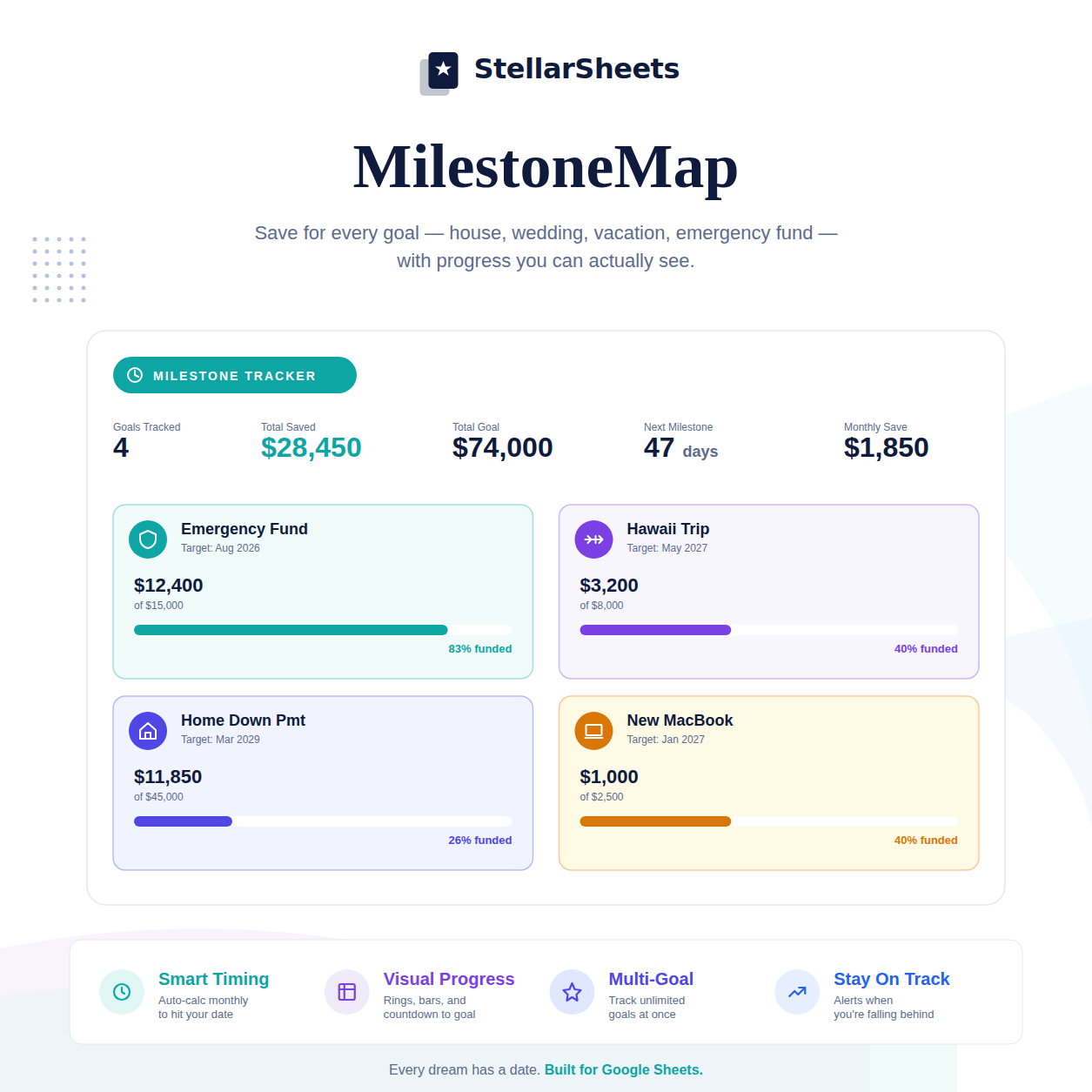

Ready to Put This Into Action?

The math behind freedom is simple. The MilestoneMap – Savings Goal Tracker tracks multiple savings goals simultaneously, shows visual progress bars, and tells you exactly how much to save each month to hit every target on schedule. Pre-built formulas, instant download, yours forever.

Or browse the full Savings & Investing Templates collection to find the right tool for your situation.

-

Posted in

budgeting, financial goals, money habits, personal finance, saving money