"Where Is All My Money Going?" 7 Hidden Money Drains in Your Budget

You're Not Broke. You're Leaking.

There's a specific kind of financial frustration that hits people who earn a decent income but never seem to get ahead. The bills are paid. The lifestyle isn't extravagant. And yet the savings account barely moves. The money goes somewhere — it always does — but where exactly is never quite clear.

This is the leaky budget problem. Not a spending problem. Not an income problem. A visibility problem. Here are the 7 most common places money leaks without anyone noticing.

1. Subscriptions You've Forgotten About

The average American underestimates their monthly subscription spend by $100–$200. Free trials that auto-converted. Apps downloaded once for a specific purpose. Streaming services added during a binge and never canceled. Annual renewals that hit once and disappear into the noise.

Fix: pull 3 months of bank and credit card statements and list every recurring charge. Cancel anything you haven't used in 30 days.

2. Food Spending (Both Kinds)

Groceries and dining out are typically the largest variable expense category — and the one with the most invisible leakage. The $4 coffee that doesn't feel like spending. The grocery run that somehow totals $180 when you went in for five things. The "quick lunch" that averages $14/day.

Fix: track food spending separately for one month. Most people are shocked by the total. Awareness alone reduces it by 15–20%.

3. Bank Fees and Interest Charges

Monthly maintenance fees, overdraft fees, out-of-network ATM fees, foreign transaction fees — these are small individually and invisible collectively. Add credit card interest on a balance you're carrying and the number gets significant fast.

Fix: review your last 3 months of bank statements specifically for fees. Switch to a no-fee checking account. Pay off the credit card balance that's accruing interest first.

4. The "Just This Once" Purchases

The one-time purchase that happens every month. The impulse buy that felt justified in the moment. The upgrade that seemed reasonable. Individually, each is defensible. Collectively, they add up to a category that never appears in anyone's budget but always appears in their bank statement.

Fix: implement a 48-hour rule for any unplanned purchase over $50. Most of them don't survive the wait.

5. Unused Gym Memberships and Wellness Subscriptions

The gym membership used twice in January and never again. The meditation app. The meal kit service that sends boxes you don't cook. The fitness tracker subscription for a device you stopped wearing.

Fix: if you haven't used it in 30 days, cancel it. You can always rejoin. You can't get back the money you spent not going.

6. Insurance You're Overpaying For

Car insurance, renters/homeowners insurance, and life insurance premiums are often set-and-forgotten. Rates change. Your situation changes. Competitors offer better rates. Most people haven't shopped their insurance in 3+ years and are paying 20–40% more than necessary.

Fix: get competing quotes for car and home insurance annually. A 20-minute phone call can save $50–$150/month.

7. The Convenience Premium

Paying for convenience is fine — when it's intentional. The problem is the convenience premium that's invisible: the grocery delivery fee plus tip plus markup on items. The airport food because you didn't pack snacks. The last-minute purchase because you didn't plan ahead. The premium streaming tier for features you don't use.

Fix: identify your top 3 convenience premiums and decide which ones are worth it. Keep those. Eliminate the rest.

The Common Thread

Every item on this list shares one characteristic: it's invisible until you look for it. The fix isn't willpower or deprivation — it's visibility. See where the money goes, decide which leaks are worth plugging, and redirect the savings toward something that actually matters to you.

Ready to Put This Into Action?

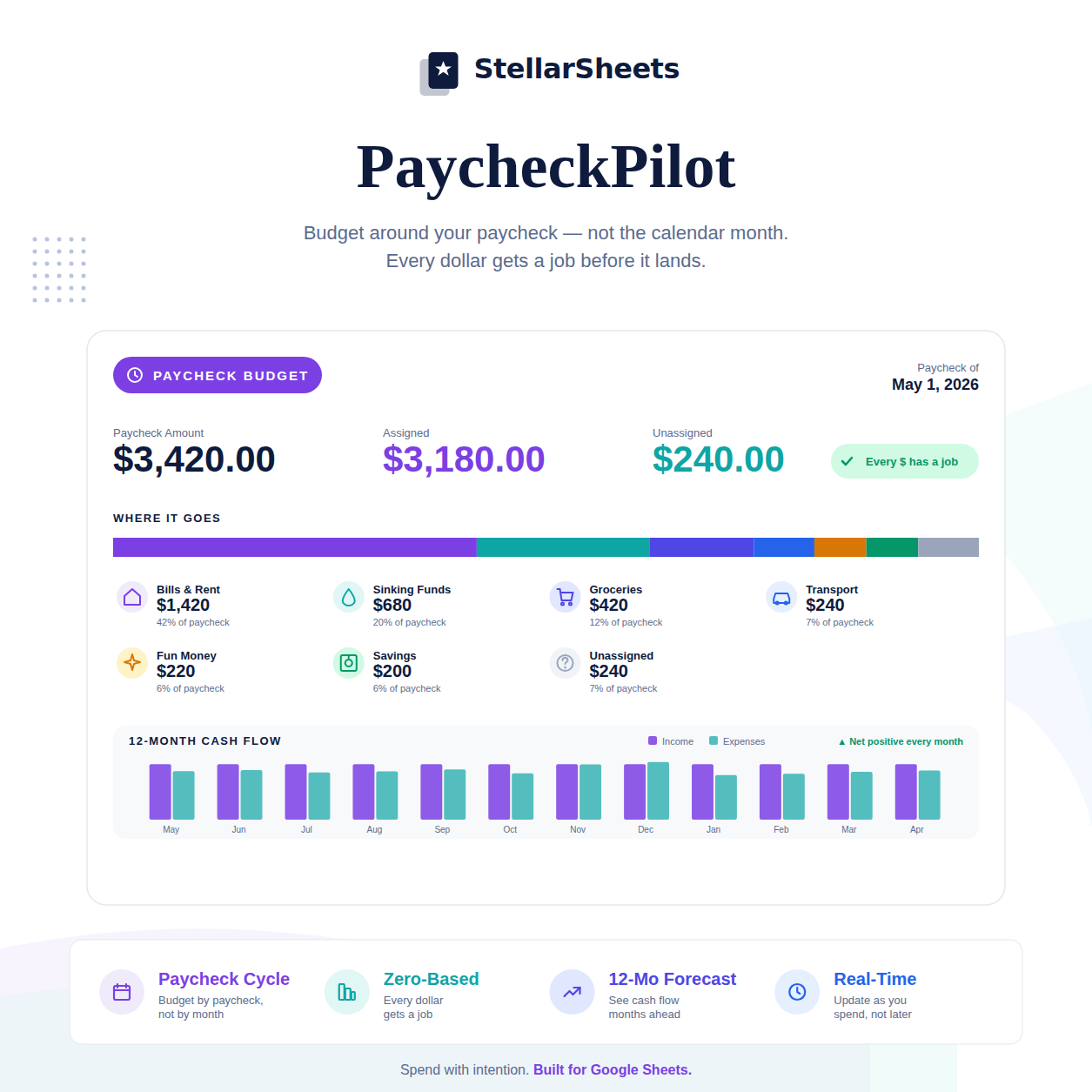

Knowing the strategy is step one. Having the right tool is step two. PaycheckPilot – Google Sheets assigns every dollar before you spend it — zero-based, paycheck-by-paycheck, with a 12-month cash flow forecast built in. Pre-built formulas, instant download, yours forever.

Or browse the full Budgeting Templates collection to find the right tool for your situation.

-

Posted in

budget tips, budgeting, money management, personal finance, save money