Savings Goal Tracker: Hit Any Target on Schedule

A Savings Goal Without a Tracker Is Just a Wish

You want to save $20,000 for a house down payment. Or $5,000 for an emergency fund. Or $3,500 for a vacation. The goal is clear. The timeline is fuzzy. The monthly contribution needed is a guess. And three months in, you're not sure if you're on track or falling behind.

That's the gap a savings goal tracker fills. Not motivation — math. Specifically: how much do you need to save each month to hit your target by your deadline, and are you currently on pace?

The Three Numbers Every Savings Goal Needs

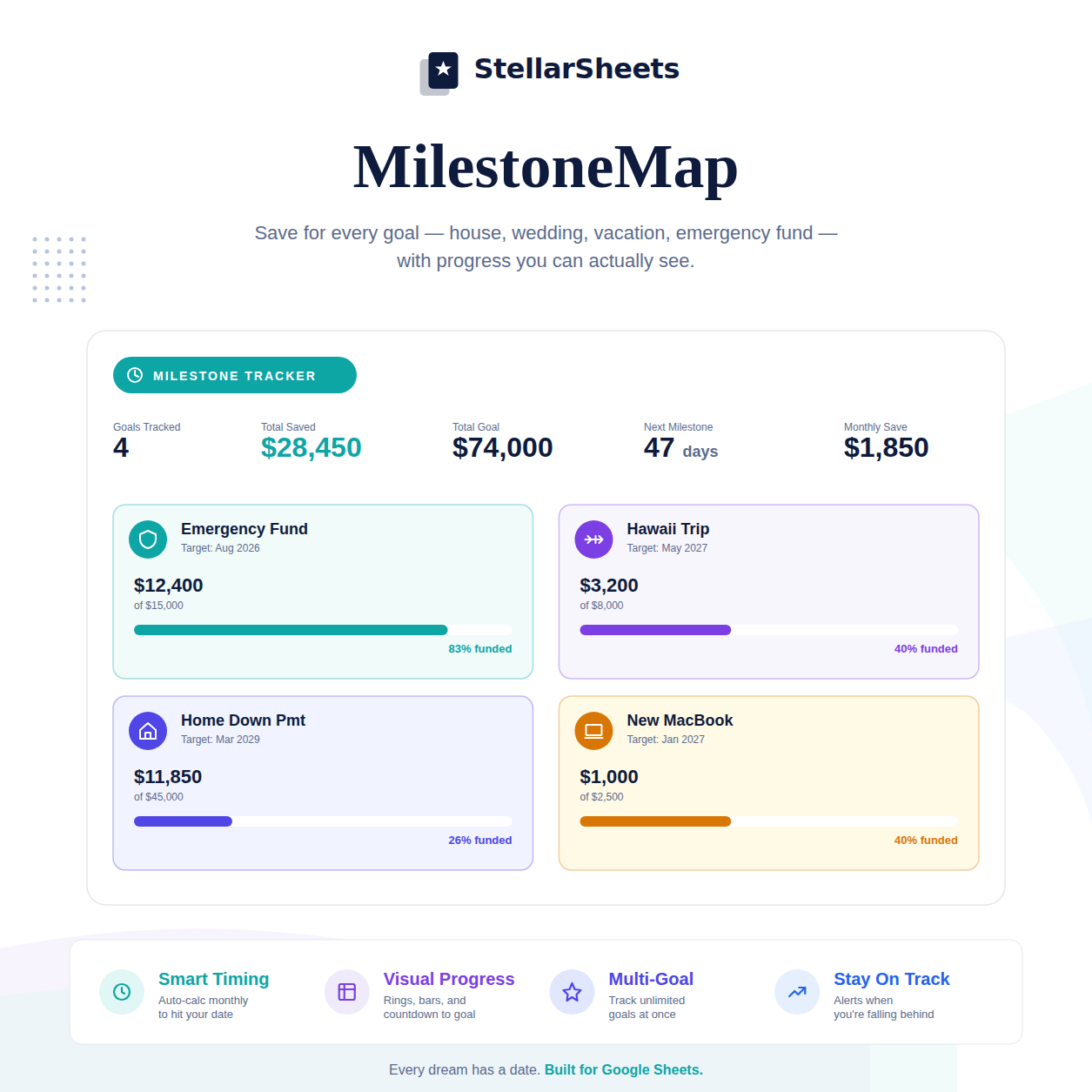

Target amount — the specific dollar figure you're saving toward. Not "a lot" or "enough" — a number.

Target date — when you need the money. A down payment closing date, a vacation departure date, a tax payment due date. Deadlines make goals real.

Monthly contribution needed — (target amount minus current savings) ÷ months remaining. This is the number that tells you whether your goal is achievable at your current savings rate — or whether you need to adjust the target, the date, or the contribution.

Why Most People Fall Behind on Savings Goals

Three reasons: no specific monthly target (so any amount feels like progress), no visibility into whether they're on pace (so falling behind goes unnoticed), and competing goals pulling from the same pool of money (so the most urgent one always wins).

A tracker fixes all three. It gives you a monthly target, shows your progress against it, and lets you run multiple goals simultaneously so you can see how they interact.

The Emergency Fund: Your First Savings Goal

Before any other savings goal, financial planners universally recommend a 3–6 month emergency fund. This is the buffer that prevents a car repair or medical bill from derailing your debt payoff plan or forcing you back into credit card debt. If you're currently living paycheck to paycheck, start with a $1,000 mini emergency fund — enough to handle most common unexpected expenses. See Paycheck-to-Paycheck No More for the full system.

Running Multiple Goals at Once

Most people have more than one savings goal at a time: emergency fund, vacation, car repair reserve, holiday gifts, down payment. Without a system, these compete invisibly. The most emotionally urgent one gets funded; the others stall.

A multi-goal tracker makes the competition visible. You can see: if I put $400/month toward the emergency fund and $200/month toward the vacation, the emergency fund hits its target in 8 months and the vacation fund hits its target in 11 months. Or: if I want both by June, I need $650/month total. Now you can make a real decision instead of a vague intention.

The Progress Bar Effect

Visual progress tracking is genuinely motivating in a way that a number in a cell isn't. Seeing a goal at 67% complete — represented as a bar, not just a fraction — triggers a different psychological response than seeing "$6,700 of $10,000 saved." Both convey the same information. One makes you want to keep going.

This is why savings trackers with visual progress indicators have better completion rates than plain spreadsheets. The design isn't cosmetic — it's functional.

Savings Goals and Your Budget

Savings goals only work if they're built into your budget as line items — not funded from whatever's left over at the end of the month. A zero-based budget assigns your savings goal contributions before discretionary spending, which is the only reliable way to ensure they actually get funded every month.

What to Do When You Fall Behind

Life happens. An unexpected expense hits, a month gets tight, a contribution gets skipped. The tracker tells you immediately: you're now $300 behind pace. You have three options: increase next month's contribution to catch up, extend the target date, or reduce the target amount. All three are valid. The tracker makes the trade-off explicit so you can choose intentionally instead of just hoping it works out.

Frequently Asked Questions

How do I calculate how much to save each month for a goal?

Subtract your current savings from your target amount, then divide by the number of months until your deadline. Example: $10,000 goal, $2,000 saved, 16 months remaining = ($10,000 − $2,000) ÷ 16 = $500/month needed.

How do I track multiple savings goals at once?

Use a multi-goal tracker that shows each goal's target, current balance, monthly contribution, and progress percentage simultaneously. This makes the trade-offs between goals visible — you can see exactly how funding one goal affects the timeline of another.

What savings goals should I prioritize?

Most financial planners recommend this order: (1) $1,000 mini emergency fund, (2) employer 401k match, (3) high-interest debt payoff, (4) full 3–6 month emergency fund, (5) Roth IRA, (6) other savings goals. Adjust based on your specific situation and interest rates.

How much should I have in an emergency fund?

3–6 months of essential living expenses — rent/mortgage, utilities, food, minimum debt payments, insurance. For people with variable income (freelancers, commission-based workers), 6 months is the safer target. Keep it in a high-yield savings account, not invested.

What's the difference between a savings goal tracker and a budget?

A budget tracks income and spending across all categories. A savings goal tracker focuses specifically on progress toward defined targets — how much you've saved, how much you need, and whether you're on pace. They work together: your budget determines how much you can contribute to savings goals each month; your tracker shows whether that contribution is enough to hit your targets on time.

Ready to Put This Into Action?

The math behind freedom is simple. The MilestoneMap – Savings Goal Tracker tracks multiple savings goals simultaneously, shows visual progress bars, and tells you exactly how much to save each month to hit every target on schedule. Pre-built formulas, instant download, yours forever.

Or browse the full Savings & Investing Templates collection to find the right tool for your situation.

-

Posted in

budgeting, google sheets, savings, savings goals, tracker